Journal Voucher in Tally Prime

A Journal Voucher is used to record non-cash and non-bank transactions in Tally Prime. It is mainly used for adjustment entries, provisions, depreciation, expense accruals, and other accounting adjustments that do not involve cash or bank. Some common uses of journal voucher in tally:

- Adjustment Entries : Outstanding Expenses, Prepaid Expenses.

- Depreciation Entries : Reducing Asset Value.

- Provision Entries : Creating provisions for tax or expenses.

- Credit/Debit Notes : Writing off bad debts.

Recording Journal Voucher:

You can use a Journal Voucher to record transaction in either Single Entry or Double Entry mode.

Journal in Double Entry Mode

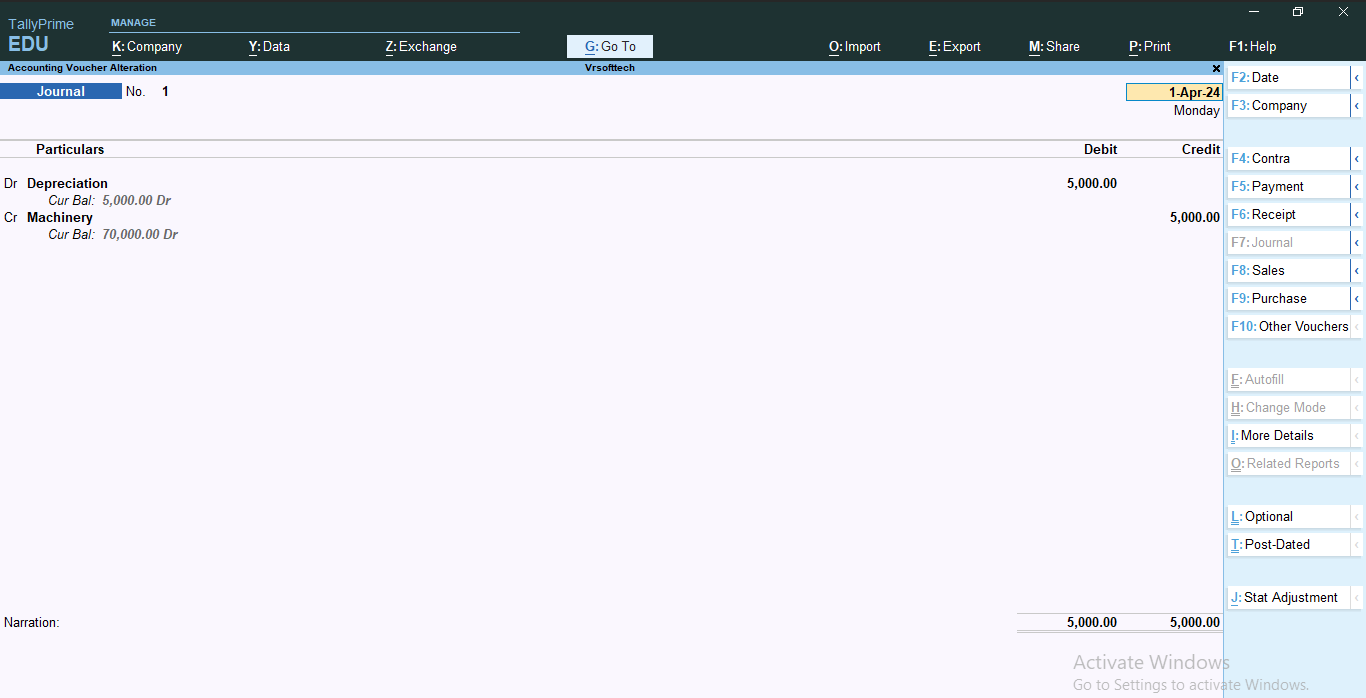

Example: A company charges ₹5,000 depreciation on Mahinery.

| Particulars |

Debit (Dr) |

Credit (Cr) |

| Depreciation A/c (Indirect Expenses) |

₹5,000 |

|

| Machinery (Fixed Asset) |

|

₹5,000 |

- In "Gateway of Tally" Window => click "Vouchers" => press F7 (Journal).

- Dr: Debit the depreciation ledger and enter the amount in Debit column.

- Cr: Credit the asset ledger and enter the amount in Credit column.

- Press Enter or click on "Yes" in the Accept Screen

- Alternatively, Press Ctrl + A to save the voucher.

Journal Entry with Examples

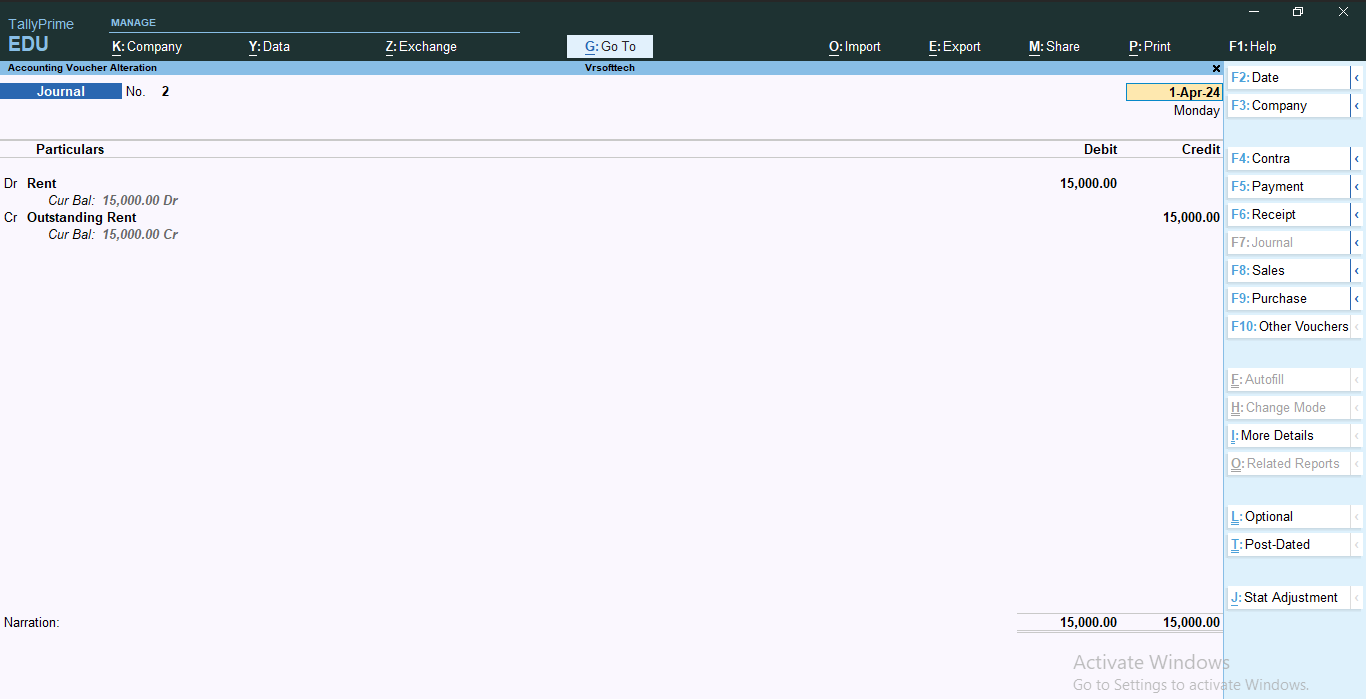

Example 1 : A company needs to record rent of ₹15,000 that is due but not yet paid. (This amount becomes an outstanding liability until paid.)

| Particulars |

Debit (Dr) |

Credit (Cr) |

| Rent A/c (Indirect Expenses) |

₹15,000 |

|

| Outstanding Rent A/c (Current liability) |

|

₹15,000 |

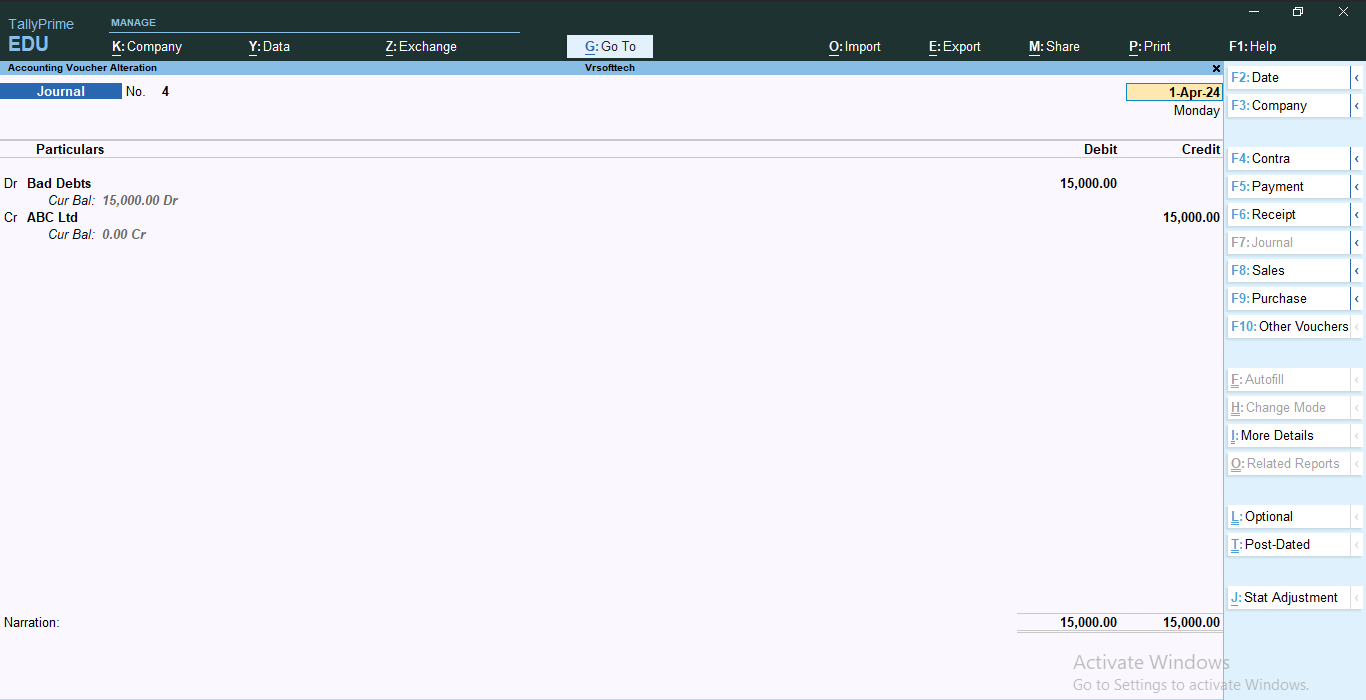

Example 2 :A customer, ABC Ltd, owes ₹15,000 but is unable to pay. The amount is written off as a bad debt.

Example 2 :A customer, ABC Ltd, owes ₹15,000 but is unable to pay. The amount is written off as a bad debt.

| Particulars |

Debit (Dr) |

Credit (Cr) |

| Bad Debts A/c (Indirect Expenses) |

₹15,000 |

|

| ABC Ltd A/c (Sundry Debtor) |

|

₹15,000 |

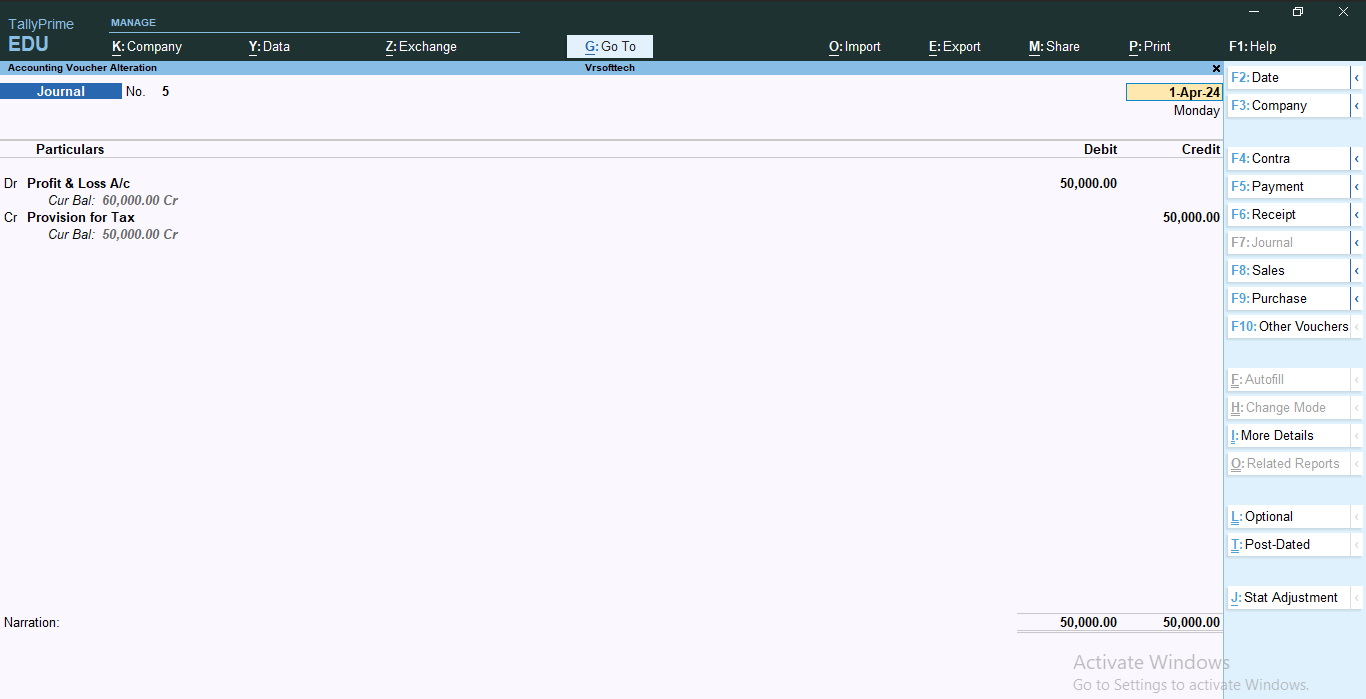

Example 3 : A company estimates a tax liability of ₹50,000 at the end of the financial year and wants to create a provision for it.

Example 3 : A company estimates a tax liability of ₹50,000 at the end of the financial year and wants to create a provision for it.

| Particulars |

Debit (Dr) |

Credit (Cr) |

| Profit & Loss A/c (P&L A/c) |

₹15,000 |

|

| Provision for Tax A/C (Current Liabilities) |

|

₹15,000 |

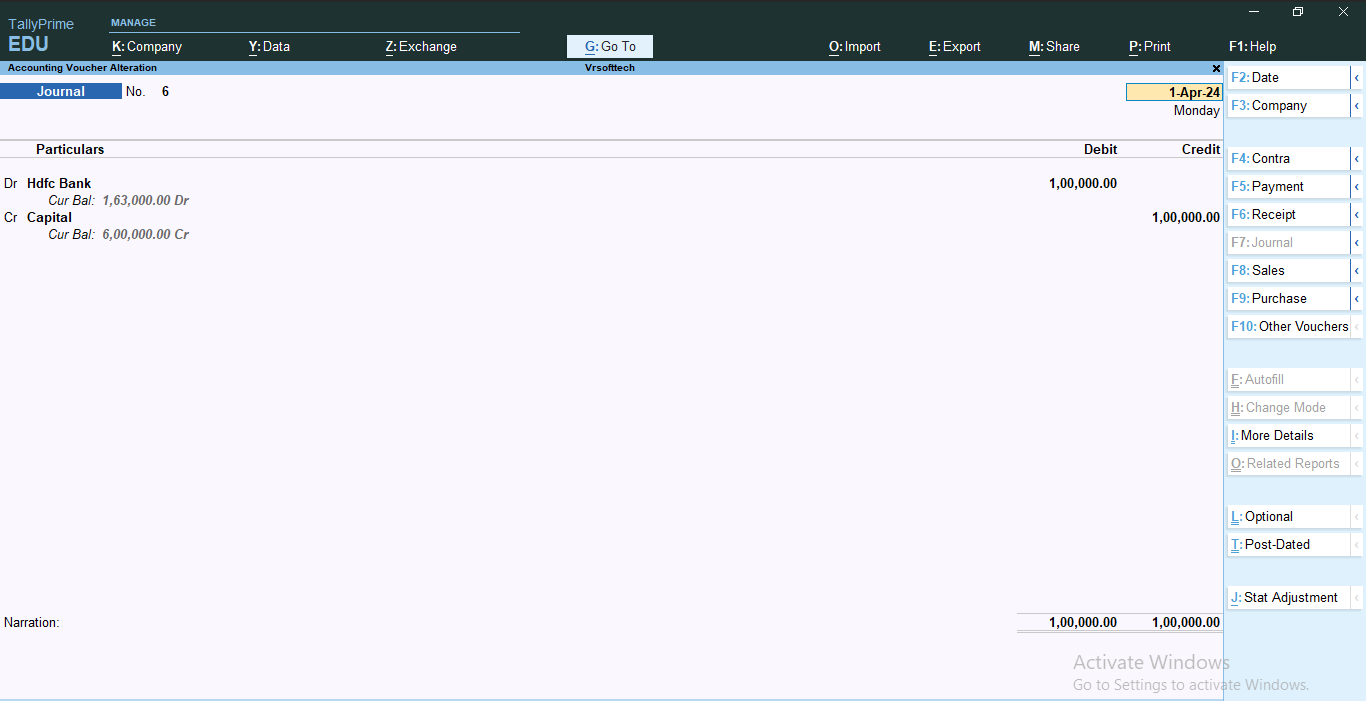

Example 4 : A company owner invests an additional ₹1,00,000 as capital into the business.

Example 4 : A company owner invests an additional ₹1,00,000 as capital into the business.

| Particulars |

Debit (Dr) |

Credit (Cr) |

| Bank A/c (Bank Account) |

₹1,00,000 |

|

| Capital A/C (Capital Account) |

|

₹1,00,000 |