Accounting Voucher in Tally Prime

Voucher is a document that contains the details of a financial transaction. Vouchers help in maintaining accurate and organized financial records. It is used to record transactions such as sales, purchases, payments, and receipts. Each voucher represents a specific transaction and contains details such as the date, parties involved, amounts, and any additional information relevant to the transaction. In Tally, different types of vouchers are available, such as:

- Payment Voucher (F5):Used to record payments made to suppliers, creditors or for expenses like rent, salaries, etc.

- Receipt Voucher (F6):Used to record receipts from debtors or for incomes like sales, services, etc.

- Journal Voucher (F7):Used to record non-cash transactions, adjustments, and transfers between ledger accounts.

- Contra Voucher (F4):Used to record transactions involving cash deposits or withdrawals into/from bank accounts or transfers between bank accounts.

- Sales Voucher (F8):Used to record sales transactions, typically issued to customers.

- Purchase Voucher (F9):Used to record purchase transactions, typically from vendors or suppliers.

- Credit Note Voucher (Ctrl+F8):Used to record credit notes issued to customers for returns or discounts.

- Debit Note Voucher (Ctrl+F9):Used to record debit notes issued to suppliers for returns or additional charges.

What is Double entry system?

The double-entry system is a fundamental principle that ensures accuracy and integrity in financial recording. This means that every transaction recorded impacts at least two accounts: a debit entry and a credit entry. The total of debit entries must always equal the total of credit entries ensuring that the accounting equation.

Assets = Liabilities + Equity

How the double entry system works?

- Debit Entries: A debit entry is recorded on the left-hand side of an account. It represents an increase in assets or expenses or a decrease in liabilities or income.

- Credit Entries: A credit entry is recorded on the right-hand side of an account. It represents an increase in liabilities or income or a decrease in assets or expenses.

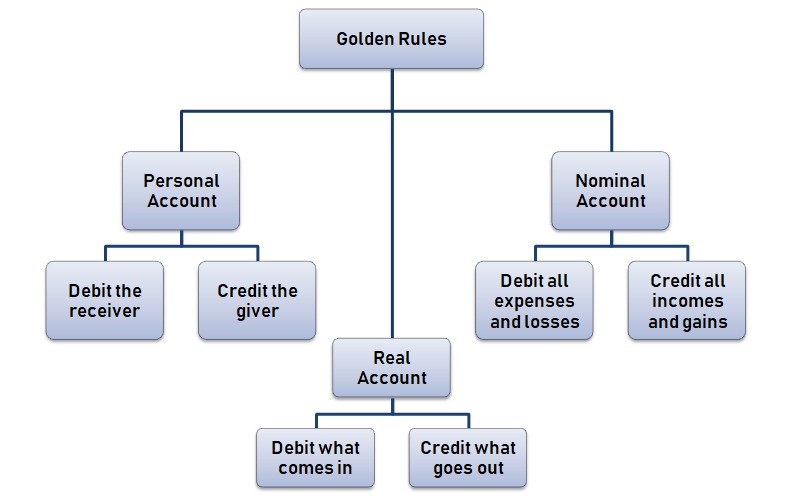

Golden Rules

For example, When you record a sales transaction

- The "sales account" is credited, reflecting an increase in revenue.

- The "debtor's account" (Accounts Receivable) is debited, reflecting an increase in assets (money owed by customers).

- The "purchase account" is debited, reflecting an decrease in revenue.

- The "creditor's account" (Accounts Payable) is credited, reflecting an increase in liability (money owed to supplier).

What is opening and closing balance?

- Opening Balance: This refers to the amount of funds or resources (like inventory, cash, etc.) available at the beginning of a financial period, such as a financial year. It is the balance carried forward from the previous accounting period.

- Closing Balance: This refers to the amount of funds or resources remaining at the end of the financial period after all transactions have been accounted for. It is the balance that is carried forward to the next accounting period as the opening balance.